Long term disability insurance provides some income protection — usually up to 60% of an employee's base salary. But it’s often capped at a lower monthly amount. Highly compensated employees who become disabled could face a large coverage gap.

Individual disability insurance can help raise the coverage amount. Plus, it can cover income earned through bonuses, distributions and other incentives. This financial protection can help you attract and retain high-earning employees.

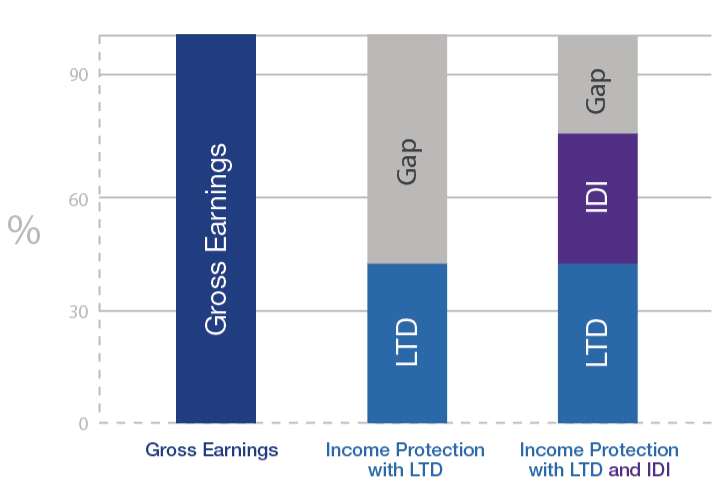

This graph assumes an LTD plan of 40% income replacement to a $10,000 monthly plan maximum, coordinating with an individual disability insurance plan design of 75% replacement to a $10,000 monthly plan maximum, for a combined coverage maximum of $20,000 between plans.

This graph is intended for illustrative purposes only.

Help Reduce the Coverage Gap

The need for income protection is greater than ever. About one in four of today’s 20-year-olds will become disabled before age 67, according to the Social Security Administration.1

Individual disability insurance offered on a guaranteed standard issue plan pays monthly benefits to individuals whose earnings are affected by an injury or sickness that keeps them from working.

Go even further to protect your employees with Platinum Advantage GSI, which includes:

- Discounted premium rates

- No medical underwriting

- Portable and individually owned policies

- Identical rates for women and men

- Coverage for employees up to age 99

- Insurance that covers incentive income

- Coverage that can grow as incomes increase

Explore the Advantages

Platinum Advantage GSI

Offer a flexible income protection plan that can meet your employees' varying needs.

Family Care Benefit

Learn more about a unique benefit for employees who miss work while caring for a child, parent or spouse with a serious health condition.